Time to Gird for Rough Times: Forecast Commentary (Part 1)

We will experience a recession by the rule of thumb metric, but this time the National Bureau of Economic Research mavens will find it difficult to define the recession by standard tools.

by Rajeev Dhawan*

A reporter friend of mine quipped after the last conference in February that I would become more pessimistic by the time I wrote my next forecast report. He has been familiar with my writings for a long time and has come to know me, so I won’t name him. So where do I stand at present? I have downgraded my GDP projections slightly for 2008 but more dramatically for 2009. I am a bit more pessimistic on the strength — or rather a lack of it — in consumer spending and the high price of oil, which will remain elevated above $100 per barrel until fall. I suspect the high price is due more to supply side issues than mere speculation. The demand side can’t be the culprit, because the global economy has slowed rather than accelerated in the past 12 months. Thus, high gas prices will blunt whatever little pop we were going to get from the rebate checks in the coming months.

The populist nature of all the presidential candidates — if it’s not a gas tax holiday scheme, then it is a threat to raise taxes on capital gains or a promise of spending cuts that just don’t exist — calls into question how desperately the two sides will pander to the electorate before November. Be assured that we will be made to feel like royalty until we cast our ballot on November 4. Then the bill for these perks will come due in later years. Be prepared for higher taxes in coming years whether at the local municipal or federal level. The final bill depends upon what taxpayers get in the coming months.

I expect real GDP growth to be negative in the next two quarters, with the current quarter falling into the deepest category. We will experience a recession by the rule of thumb metric, but this time the National Bureau of Economic Research (NBER) mavens will find it difficult to define the recession by standard tools. Luckily, job losses will be mild by historical standards, as the corporations have little fat to cut. The latest job recovery period lasted barely four years, and all the bloating happened in real estate and its enabling sectors (mortgage brokers, banks, and Wall Street shops). These sectors already were paring jobs for the past year. And approximately one-half of the economy by employment base — Hospitality, Education and Healthcare, and Government sectors — actually added 300,000 jobs when the economy lost more than a quarter million jobs overall. Still, the recovery will be a drawn-out affair. Only in late 2009 will we see some respectful quarters of growth. Therefore, after growing by 2.2% in 2007, the economy will grow only 0.9% in 2008 and then again an anemic 1.0% in 2009. Normalcy returns in 2010 when the economy will grow by 2.5%. This is neither a V-shaped nor a U-shaped recovery, rather a \___/ (an obese U)!

I am a bit more pessimistic on the strength — or rather a lack of it — in consumer spending and the high price of oil, which will remain elevated above $100 per barrel until fall.My pessimism is driven by data rather than a natural progression. In fact, in mid-March when Bear Stearns was imploding, my pessimism reached its highest level since the credit crunch started last August. The Fed-engineered takeover of Bear Stearns by JP Morgan showed the decisive nature with which the Fed acted to curb a bank run. Walter Bagehot, the noted English journalist and a developer of central banking theory in the mid-19th century, had advice for a situation of this type: lend freely but at a penalty. The conduit here was JP Morgan (with the central bank putting skin in the game), but the action was decisive.

The shareholders of Bear Stearns took a bath, but at the same time, maybe the bond holders got only a slight soaking. Of course, this call is all Monday-morning quarterbacking. We can debate whether letting the bank fail would or would not have unraveled the modern financial system, but why take that risk? Currently, the economic environment is not strong like it was in 1999, where a hit to the system could be absorbed by consumers. Consumers are also voters, and they will let leaders know, based on their immediate pain, what they think of the Fed’s policy of laissez faire at the next fundraiser. Representative and Senator, don’t let the door hit you on the way out!

There is concern in some circles that Bank of America is grumbling that it looks like a chump in agreeing to bail out or buy Countrywide Financial all on its own dime, whereas JP Morgan got a $30 billion check from the Fed. If the BOA decides to come to the Fed, then what? If they give in to BOA, then others will demand it, too. Soon no deal will be done without the Fed as an equity partner. This problem is a moral hazard that will have to be dealt with in coming years, but it’s better to be tough now and say no than to do it later. As Milton Friedman famously quipped, “There is no such thing as a free lunch.”

One good result of the Bear Stearns episode is that some confidence is creeping back into the financial system. A good sign, for example, is the rise in the 2-year and 10-year bond yields since March 17. The 2-year yield is up by almost 100 basis points, and the 10-year is up by 60 basis points. Therefore, the Fed’s action to open its discount window to Wall Street banks and other non-interest rate interventions (such as Term Securities Lending Facility) have arrested the flight to safety in the credit markets. However, the situation has not normalized yet. The credit market spreads, especially that of LIBOR over the funds rate and AA minus A2 asset-backed commercial paper, are still abnormally high. However, they haven’t worsened since mid-March.

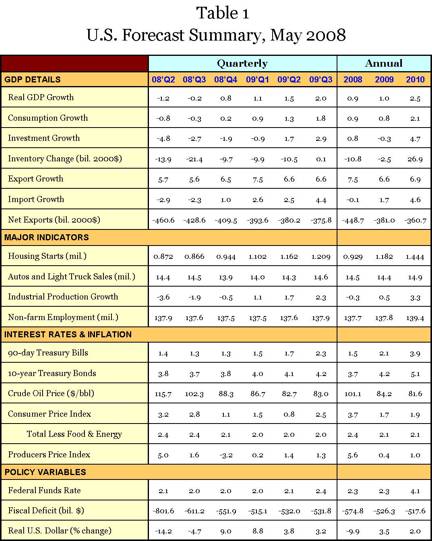

But one trend that is clearly worsening is the tendency of banks to hold back on loans to consumers. Figure 1 shows the net percentage of banks that reported tightened lending standard for residential mortgages and consumer loans. The current tightness is much more severe than what we saw in the last recession. It is not surprising that the sharpest rise has been in the mortgage loan market. The sharp jump since mid-2007 is already putting a damper on the consumers’ desire to spend. The elevated gas prices also are making a dent. Therefore, consumption growth will be absent in the coming few quarters and will not get close to 2.0% until late 2009. More details about the forecast are available in Table 1.

(Continued in Part 2)